Domestic market analysis

Products: In February, the operating rate of domestic polysilicon manufacturers remained at around 70%. The inventory was sufficient and the downstream PV industry developed rapidly. The market for the upstream polysilicon raw materials market was improving. The price of polysilicon market rose sharply, and the market turnover was also higher than the previous period. increase. At present, the annual production capacity of Chongqing Daxin Energy Solar-grade polysilicon plant is 8,000 tons. At present, the device is normally driven, and the factory price is 120,000 yuan/ton. The shipment is normal.

Industry chain: In February, the market of silicon block raw materials went up as a whole, which caused certain cost pressure on polysilicon manufacturers; the demand for downstream enterprises increased, and the photovoltaic industry in various regions of China was steadily advancing. The photovoltaic industry was in the process of rapid expansion and expansion. Among them, it is expected to drive investors' enthusiasm for investment in the domestic polysilicon market.

Industry: At present, most domestic polysilicon manufacturers are operating at full capacity, the market supply is sufficient, and the market negotiation atmosphere is getting better; the policy aspect effectively limits the number of polysilicon imports and adds momentum to the domestic polysilicon market. However, domestic polysilicon production technology has been unable to break through barriers, and the production cost is relatively large, which limits the profit margin of domestic polysilicon manufacturers. In the long run, with the introduction of favorable national policies and the encouragement of technological innovation, the domestic polysilicon market is expected to usher in rapid development.

Market outlook

Polysilicon analysts of the business division's chemical branch believe that the current domestic polysilicon market is beginning to stabilize. Driven by downstream demand, it is expected that the polysilicon market will maintain a stable market in March.

Related reading: Domestic polysilicon market review and outlook for the market in January-February 2016

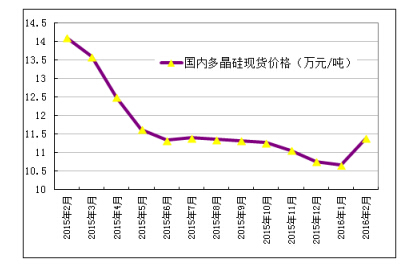

First, the price of polysilicon has steadily rebounded

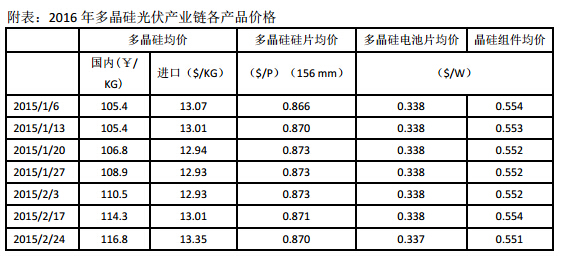

In January-February 2016, the price of polysilicon showed a “steadily rising†trend. The transaction price rebounded from the historical low of 105,400 yuan/ton at the beginning of January to the end of February at RMB 116,800/ton, an increase of 10.8%. The main reason for pushing up the price of polysilicon in January is: on the one hand, due to the Spring Festival, due to the Spring Festival logistics and transportation, downstream silicon companies hoard stocks in advance to ensure production supply during the Spring Festival, and on the other hand, the middle and lower reaches are optimistic about the terminal in the first half of the year. The installation market and the expansion of production capacity were gradually released, which led to an increase in demand for polysilicon in January, which led to a slight rebound in polysilicon prices. The main reason for supporting the rebound in polysilicon prices in February was that most of the enterprise orders before the lunar calendar had been signed to the end of February, and there was no excess inventory in the hands. Therefore, the quotations continued to rise after the Spring Festival, and the maximum price of polysilicon reached 122,000 yuan/ton by the end of February. The mainstream transaction price also rebounded to 11.151.8 million yuan / ton, the highest has a turnover of 120,000 yuan / ton, the new order delivery period continues to be extended to March, therefore, the strong demand for polysilicon is the main driving factor to stimulate prices continue to pick up .

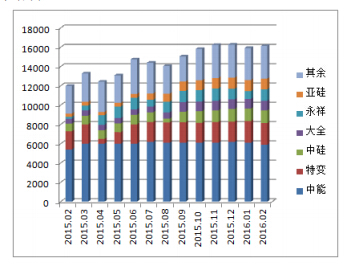

According to statistics from the Silicon Industry Branch, domestic polysilicon production in January-February 2016 was 32,000 tons, a significant increase of 34.5% year-on-year. In January, the output was 15.9 million tons, and the output in February was 161,000 tons. Among them, Jiangsu Zhongneng's output accounted for 37.4% of the total output in January-February, which accounted for a decrease in the proportion, but still ranked first in domestic production. The special change and Luoyang Zhongsi ranked second and third respectively, and the top three enterprises ranked by output in January-February accounted for 59.6% of the total output. During the January-February period, some enterprises (Sichuan Yongxiang, Yichang CSG, Shenzhou Silicon, etc.) were affected by circuit problems or maintenance technical changes, and the production capacity was not full. The rest of the enterprises maintained full production. At present, there are 14 production enterprises, of which 6 have effective production capacity of over 10,000 tons/year, and the monthly average production is over 1,000 tons/month. The advantage in market competition is slightly obvious.

Since the beginning of March 2014, polysilicon prices have experienced a continuous decline in the past two years, mainly due to the impact of the uncertainties in domestic PV policies, the slow start of downstream applications and the “processing trade assault import†triggered by the announcement of “suspension of processing tradeâ€. Domestic polysilicon demand has been significantly reduced, and the polysilicon industry has suffered severely. However, due to the dual pressures of foreign import volume and price, domestic polysilicon enterprises have to produce or even expand production in order to reduce costs, and in 2014, the sudden import of imports led to a large backlog of inventory. Continued to 2015, resulting in new inventory in 2015 reached about 35,000 tons. Until 2016, benefiting from the expectations of midstream and downstream enterprises for terminal photovoltaic power plants, the production capacity of silicon wafers, battery chips and components has expanded significantly. Coupled with the strong willingness to stock up before the Lunar calendar, the demand for polysilicon has suddenly increased, and the inventory is in 2016. At the end of January of the year, it was completely digested and continued until the end of February. There were no excess stocks in the hands of domestic polysilicon enterprises.

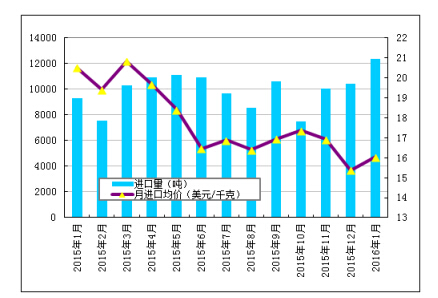

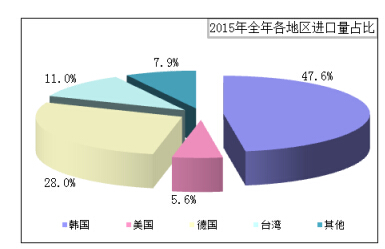

Third, the import volume of polysilicon has reached a new high, and Hantai is still the main driving force.

According to the latest statistics from the customs, China's polysilicon imports reached a record high in January 2016, reaching 12,388 tons, an increase of 18.6% from the previous month. Mainly due to the high level of imports of polysilicon from South Korea and Taiwan: First, South Korea's imports reached a record high for two consecutive months, with a record high of 5,897 tons in January, an increase of 11.5% from the previous month, accounting for 47.6% of the total imports of the month. It still maintains the largest source of imports, which is 70.1% higher than the second-ranked German import, even surpassing the total imports of each country in the previous year, and the degree of dumping is increasing. Second, in January, 1,358 tons of polysilicon was imported from Taiwan, accounting for 11.0% of the total imports, ranking the third largest import region in China for more than half a year. It is precisely because the way of evading the “double-reverse†taxation through Taiwan’s imports has gradually become the mainstream, so even if the US imports are greatly reduced, the sum of imports from the United States and Taiwan is also around 1500-2000 tons/month, and the United States has not decreased. It was no different before, so the fact that Taiwan’s re-exports remained high was also another major factor leading to high silicon imports.

In January, the average price of polysilicon imports rebounded slightly to US$16.04/kg, a 4.3% increase from the previous month, mainly due to a significant increase of 105% from the US in January to US$43.67/kg, a record high. The analysis is mainly subject to “ The impact of the double-reverse "punitive tariffs", the number of spot orders imported from the United States has been greatly reduced, and the proportion of long-term orders has increased, resulting in a sharp increase in the average price of imports from the United States. And Hande's import prices are all low: after importing prices from South Korea for nine consecutive months, it continued to hit a record low of US$12.99/kg in January, down 36.0% year-on-year; Germany also hit a record low of US$15.54/ Kilograms, down 33.8% year-on-year.

Behind the policy continues to help, China's photovoltaic industry has already emerged from the haze in 2015, and the fundamentals are warming up. According to public information, in 2015, China's new PV installed capacity was about 15GW, up 41% year-on-year, ranking first in the world for three consecutive years, of which ground-based power plants accounted for 84%, distributed power plants accounted for 16%, and the country's cumulative installed capacity was about 43GW. Leap to the top in the world.

This hot trend can be further confirmed by the financial reports of listed companies. Nearly 30 of the 37 solar power concept companies released their 2015 annual results forecast, and 18 achieved net profit growth year-on-year, of which 15 are expected to grow by more than 50%. Weiwei shares topped the list with 1490.16%-1519.51%. After that, Aerospace Electromechanical Co., Ltd. is expected to increase its net profit by 382%-415%. Affected by this, the profitability of midstream component companies has also improved significantly. The average capacity utilization rate of 51 component companies was 86.7%, which was 6 percentage points higher than the first half of 2015. The profit margins of the top ten companies are mostly in double digits. After analyzing the 2015 operating performance of 33 companies that have passed the standard conditions (the statistics exclude several companies that have suffered losses due to excessive historical burden), only 4 companies The company's loss, the average profit margin reached 4.8%, significantly higher than the 3% average of the electronics manufacturing industry, and also higher than the 2-3 percentage points in the first half of 2015.

In 2016, the National Energy Administration issued two regulations on photovoltaic power generation in January alone. The introduction of the policy has played a positive role in the recovery of the entire photovoltaic industry. It is estimated that the new wafer production capacity will reach 8-9GW in 2016, and the new capacity of battery chips and components will reach 8-9GW and 12-14GW respectively. The annual installed capacity of PV will reach 20GW. The growth rate of new capacity of downstream enterprises was obvious, and the demand for polysilicon was significantly increased. As of the end of February 2016, the average monthly demand for polysilicon reached 26,000 tons/month, which was 0.4 million tons/month higher than the average monthly demand at the end of 2015. That is to say, the newly released capacity of wafers in February actually reached 0.8GW/month, and the new capacity in the downstream chain will continue to be gradually released.

V. Polysilicon market outlook

According to the end of 2015, the output of polysilicon was 169,000 tons, the import was 117,000 tons, the export was 0.7 million tons, the electronic grade was 0.3 million tons, and the polysilicon used for wafer production was 250,000 tons. The surplus was 26,000 tons in 2015, and the downstream polysilicon inventory was 0.9 million tons. That is, the total new inventory in 2015 was about 35,000 tons. In January, domestic polysilicon production was about 16,000 tons, and imports were estimated at 12,000 tons. That is, the supply increased by 28,000 tons in January. In view of the fact that polysilicon enterprises have no stock at all, the supply of 63,000 tons will be transferred to the downstream as of the end of January. Excluding the downstream normal demand of 26,000 tons / month (after the downstream capacity increase) and the stock of 20,000 tons (optimistic estimate), there are 11,000 tons remaining, which may be the increase in demand due to the expansion of new wafer capacity However, it is also possible that the downstream stocks have exceeded the normal amount, and signs of the stoppage of the price of silicon wafers from the end of February can also be indicated. With the gradual implementation of terminal power plant installation requirements, polysilicon supply demand will gradually balance, and prices are expected to stabilize until the end of March.

Basin Tap

Bestware Basin Tap brings the fine design and high technology together in all areas of the product process beyond Pull Out Faucet, Commercial Faucet and Commercial Kitchen Faucet. With extensive range of components, we can offer a large selection of both standard Pre-rinse Faucet and custom Mixer Tap units as well as flexible combination. Stainless steel is 100% recyclable and is comprised of over 60% recycled material, Bestware faucets are the perfect solution in the commercial and industry for better water quality and the circumvention of the development of deleterious substances and bacteria. No plating, no oxidizing, no rust, lead free.

Basin Tap,Bathroom Sink Taps,Bathroom Mixer Taps,Bathroom Basin Taps

Bestware Hardware Production Co., Ltd. , https://www.bestwarefaucets.com